Taiwanese IT Suppliers Seek Paydirt in Auto Electronics

Sep 08, 2005 Ι Industry News

Ι Electronics and Computers Ι By Ken, CENS

When Chairman S.H. Hsu of the Taiwan Electrical and Electronic Manufacturers' Association (TEEMA) recently said his enterprise, Kinpo Group, would plunge into the automotive electronics business, he was serving as a reflection of the reality that most of his industry peers are looking for new applications to escape the information-technology (IT) manufacturing slump.

Gross margins in Taiwan's IT industry, insiders say, have averaged a mere 5% over the past few years, far below the double-digit earnings of the past. Citing a study by Gartner, James Huang, a market research fellow at the Industrial Economics and Knowledge (IEK) Center of the government-backed Industrial Technology Research Institute (ITRI), says that the world computer-chip market rose about 24.8% last year, a significant drop from 40% or so gains before 2001. "This and next year, computer-chip market will only present a single-digit growth pace," he estimates.

Huang attributes the sluggish growth rate mostly to weak demand for replacement desktop computers--the largest application for semiconductors.

"Taiwan's IT-equipment suppliers need to identify the next fast-growth applications," says Hsu, whose association represents over 4,000 Taiwanese electronics and electrical equipment suppliers. One such area, he says, is cars.

Gearing Up

According to Huang, the automotive semiconductor market rose 14.8% last year and will continue to maintain steady growth over the next few years. "Although automotive semiconductors now account for barely 10% of world semiconductor market, their market will grow steadily," he says.

Executives of European chipmaker Infineon Technologies AG's automotive and industrial business unit forecast that manufacturers will build US$290 billion worth of electronic components and devices into vehicles by 2020, more than double the 2001 figure of US$134 billion. The semiconductor portion of that figure was estimated at US$11.7 billion in 2001, and it is projected to reach US$21.4 billion by 2020.

IC Insights predicts that the average electronics content of cars will soar to 40% by 2010 from today's 26%. Strategy Analysis estimates that the markets for telematics and electronics for chassis, suspension, auto body, safety, security and power transmissions will grow at compound average growth rates of between 5% and 11.9% between 2003 and 2008.

Japanese market-research organization SRD forecasts that cars in Europe, United States, and Japan equipped with telematics system, a device that combines telecommunications systems with computers, to increase to 22.2 million vehicles next year from 2004's 13.87 million vehicles.

Hsu points out that the electronics content of cars is about 25% in Asian cars and 40% in European models. "The content ratio will continue to grow, and the closed supply chains of automotive electronics will become open to global suppliers. This is an area that Taiwanese IT companies should be seriously considering," he says.

According to automotive-chip supplier Microchip Technology of the United States, American carmakers will begin adding microcontrollers into their cars from 2006 to control motor speed, tire temperature and pressure, and car radar systems.

Former Vice Premier Lin Hsin-I believes that the automotive-electronics industry will be the next battlefield for the world's IT suppliers. Taiwanese suppliers, he says, can win in the rising segment if they are well prepared.

Roadblocks

Much of this preparation means having the ability to meet the strict safety requirements placed on automotive electronics and breaking into the relatively closed supply chains in this sector. Most of the world's leading carmakers buy electronics exclusively from suppliers with which they work closely. GM, Ford, Toyota, Daimler-Chrysler, Renault-Nissan, and Volkswagen have Delphi, Visteon, Denso, Autolive, Robert Bosch and Siemens VDO, respectively.

Taiwan's electronics and electrical equipment suppliers took action early this year by forming an automotive electronics committee under Hsu's association, which now has 18 industrial committees. The association's president, Joseph Cheng, coordinated the formation with Chintay Shih, a former ITRI President. "The committee is set up to facilitate the formation of an industry cluster for Taiwan's auto-electronics business. With the collective strength, we can cut into the field as quickly as possible," Cheng says.

The committee's strategy, Cheng notes, is to tap original equipment (OE) manufacturing opportunities in mainland China and the aftermarket (AM) sector in Taiwan. The mainland churned out five million cars last year and is estimated to produce close to six million cars in 2005, providing sufficient scale to nurture Taiwan's automotive electronics industry.

"Although the mainland Chinese market has lured many Western auto-electronics suppliers, most mainland automakers are still short of experiences in the auto-electronics manufacturing since the electronics industry there is still embryonic. That is our chance. We can play an intermediary role between the mainland's carmakers and western electronics suppliers, turning their electronics products into products that mainland carmakers can understand," Cheng notes.

To tap this opportunity, Hsu led 40 of his organization's members to visit an auto and auto parts forum held in Qingdao of mainland China in April this year. At this forum, he met with the mainland's auto-industry regulators and representatives from English, American, Italian, German and mainland carmakers.

Back in Taiwan, annual demand for new cars is estimated at 500,000 vehicles, but there are around six million cars on the roads, increasing the appeal of the AM auto-electronics market, Cheng says.

Strong Cards

Although the challenges are many, Taiwan has several strong cards in tapping the auto electronics business. Among them, says Cheng, are well-developed microelectronics and consumer-electronics industries and complete electronics supply chains. The trick, he says, is to link Taiwan's electronics suppliers with carmakers.

Cheng predicts that electronics parts will account for 60% of a car's cost structure in 2015, up from 40% in 2010 and 20% last year. "Some Japanese carmakers plan to introduce vehicles in which electronic systems constitute 60% of the total cost structure," he says.

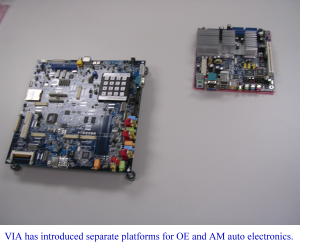

Chipset vendor VIA Technologies is viewed as Taiwan's first IT supplier to diversify into auto electronics business. The company has worked out its own auto-electronics strategies for both the AM and OE segments. Its embedded platform division is in charge of the AM market, while its multimedia consumer electronics unit focuses on OE business.

Justin Hsu, executive assistant to VIA's chairman, says his company will avoid the safety certification hurdle by focusing first on electronic devices for applications in which safety is not an issue, such as GPS (global positioning system) and entertainment systems.

VIA's embedded platform division provides computer motherboards equipped with its X86-compatible central processing unit (CPU) Eden for applications for current car models, while its multimedia consumer electronics unit is developing applications for future cars models.

The company entered the auto-electronics business around three years ago by accident. In the beginning, its embedded platform division developed platforms for industrial computers, according to Hsu, who is charge of the development of VIA's auto-electronics strategy. "At that time, we shrank the standard 21cm x 29cm PC motherboards to the 17cm x 17cm specification for industrial computers. Shortly, some system suppliers developed car-used computers around our platform," Hsu recalls. Today, the size is the standard for industrial computers.

On the board are standard devices including chipsets, CPUs, south-bridge chips and north-bridge chips.

The company's multimedia consumer electronics unit is developing a smaller platform in cooperation with an unnamed local carmaker. The platform includes a system-on-chip that incorporates CPU, north-bridge chip and south-bridge chip functions on it, enabling the board to be shrunk to 10cm x 10cm in dimension. "This size," Hsu notes, "enables the system built on the board to easily fit into car-stereo casing." The computer system is built around reduced instruction set computer (RISC) structure, allowing all commands it processes to run faster than in complex instruction set computer (CISC) model.

Hsu notes that auto-specific computers require higher reliability than do desktop and notebook PCs, as their smaller size leads to rapid heat buildup. "Heat tends to cause a computer crash if the dissipation design is not good. But a dissipation fan is usually a space killer. So, we have developed chips that eliminate the need for a dissipation fan. Our Eden chip, for example, can run at one gigahertz and does not need a fan," he says.

Hsu explains that his company has become involved in the auto-electronics business because it is a much more specialized, and thus profitable, market than the PC business.

VIA expects revenue from its auto-electronics business to top US$3 million, and possibly US$4 million, this year.

The lucrative market potential of the auto segment has also lured United Microelectronics Corp. (UMC), currently the world's second-largest wafer foundry, to acquire a 50% stake in BCOM Electronics Inc., which specializes in audio and video systems for cars. After eight consecutive years in the red, BCOM began to turn a profit in 2003 after diversifying into the auto-electronics business four years ago. (May 2005)

Huang attributes the sluggish growth rate mostly to weak demand for replacement desktop computers--the largest application for semiconductors.

"Taiwan's IT-equipment suppliers need to identify the next fast-growth applications," says Hsu, whose association represents over 4,000 Taiwanese electronics and electrical equipment suppliers. One such area, he says, is cars.

Gearing Up

According to Huang, the automotive semiconductor market rose 14.8% last year and will continue to maintain steady growth over the next few years. "Although automotive semiconductors now account for barely 10% of world semiconductor market, their market will grow steadily," he says.

Executives of European chipmaker Infineon Technologies AG's automotive and industrial business unit forecast that manufacturers will build US$290 billion worth of electronic components and devices into vehicles by 2020, more than double the 2001 figure of US$134 billion. The semiconductor portion of that figure was estimated at US$11.7 billion in 2001, and it is projected to reach US$21.4 billion by 2020.

IC Insights predicts that the average electronics content of cars will soar to 40% by 2010 from today's 26%. Strategy Analysis estimates that the markets for telematics and electronics for chassis, suspension, auto body, safety, security and power transmissions will grow at compound average growth rates of between 5% and 11.9% between 2003 and 2008.

Japanese market-research organization SRD forecasts that cars in Europe, United States, and Japan equipped with telematics system, a device that combines telecommunications systems with computers, to increase to 22.2 million vehicles next year from 2004's 13.87 million vehicles.

Hsu points out that the electronics content of cars is about 25% in Asian cars and 40% in European models. "The content ratio will continue to grow, and the closed supply chains of automotive electronics will become open to global suppliers. This is an area that Taiwanese IT companies should be seriously considering," he says.

According to automotive-chip supplier Microchip Technology of the United States, American carmakers will begin adding microcontrollers into their cars from 2006 to control motor speed, tire temperature and pressure, and car radar systems.

Former Vice Premier Lin Hsin-I believes that the automotive-electronics industry will be the next battlefield for the world's IT suppliers. Taiwanese suppliers, he says, can win in the rising segment if they are well prepared.

Roadblocks

Much of this preparation means having the ability to meet the strict safety requirements placed on automotive electronics and breaking into the relatively closed supply chains in this sector. Most of the world's leading carmakers buy electronics exclusively from suppliers with which they work closely. GM, Ford, Toyota, Daimler-Chrysler, Renault-Nissan, and Volkswagen have Delphi, Visteon, Denso, Autolive, Robert Bosch and Siemens VDO, respectively.

The committee's strategy, Cheng notes, is to tap original equipment (OE) manufacturing opportunities in mainland China and the aftermarket (AM) sector in Taiwan. The mainland churned out five million cars last year and is estimated to produce close to six million cars in 2005, providing sufficient scale to nurture Taiwan's automotive electronics industry.

"Although the mainland Chinese market has lured many Western auto-electronics suppliers, most mainland automakers are still short of experiences in the auto-electronics manufacturing since the electronics industry there is still embryonic. That is our chance. We can play an intermediary role between the mainland's carmakers and western electronics suppliers, turning their electronics products into products that mainland carmakers can understand," Cheng notes.

To tap this opportunity, Hsu led 40 of his organization's members to visit an auto and auto parts forum held in Qingdao of mainland China in April this year. At this forum, he met with the mainland's auto-industry regulators and representatives from English, American, Italian, German and mainland carmakers.

Back in Taiwan, annual demand for new cars is estimated at 500,000 vehicles, but there are around six million cars on the roads, increasing the appeal of the AM auto-electronics market, Cheng says.

Strong Cards

Although the challenges are many, Taiwan has several strong cards in tapping the auto electronics business. Among them, says Cheng, are well-developed microelectronics and consumer-electronics industries and complete electronics supply chains. The trick, he says, is to link Taiwan's electronics suppliers with carmakers.

Cheng predicts that electronics parts will account for 60% of a car's cost structure in 2015, up from 40% in 2010 and 20% last year. "Some Japanese carmakers plan to introduce vehicles in which electronic systems constitute 60% of the total cost structure," he says.

Chipset vendor VIA Technologies is viewed as Taiwan's first IT supplier to diversify into auto electronics business. The company has worked out its own auto-electronics strategies for both the AM and OE segments. Its embedded platform division is in charge of the AM market, while its multimedia consumer electronics unit focuses on OE business.

Justin Hsu, executive assistant to VIA's chairman, says his company will avoid the safety certification hurdle by focusing first on electronic devices for applications in which safety is not an issue, such as GPS (global positioning system) and entertainment systems.

VIA's embedded platform division provides computer motherboards equipped with its X86-compatible central processing unit (CPU) Eden for applications for current car models, while its multimedia consumer electronics unit is developing applications for future cars models.

The company entered the auto-electronics business around three years ago by accident. In the beginning, its embedded platform division developed platforms for industrial computers, according to Hsu, who is charge of the development of VIA's auto-electronics strategy. "At that time, we shrank the standard 21cm x 29cm PC motherboards to the 17cm x 17cm specification for industrial computers. Shortly, some system suppliers developed car-used computers around our platform," Hsu recalls. Today, the size is the standard for industrial computers.

On the board are standard devices including chipsets, CPUs, south-bridge chips and north-bridge chips.

The company's multimedia consumer electronics unit is developing a smaller platform in cooperation with an unnamed local carmaker. The platform includes a system-on-chip that incorporates CPU, north-bridge chip and south-bridge chip functions on it, enabling the board to be shrunk to 10cm x 10cm in dimension. "This size," Hsu notes, "enables the system built on the board to easily fit into car-stereo casing." The computer system is built around reduced instruction set computer (RISC) structure, allowing all commands it processes to run faster than in complex instruction set computer (CISC) model.

Hsu notes that auto-specific computers require higher reliability than do desktop and notebook PCs, as their smaller size leads to rapid heat buildup. "Heat tends to cause a computer crash if the dissipation design is not good. But a dissipation fan is usually a space killer. So, we have developed chips that eliminate the need for a dissipation fan. Our Eden chip, for example, can run at one gigahertz and does not need a fan," he says.

Hsu explains that his company has become involved in the auto-electronics business because it is a much more specialized, and thus profitable, market than the PC business.

VIA expects revenue from its auto-electronics business to top US$3 million, and possibly US$4 million, this year.

The lucrative market potential of the auto segment has also lured United Microelectronics Corp. (UMC), currently the world's second-largest wafer foundry, to acquire a 50% stake in BCOM Electronics Inc., which specializes in audio and video systems for cars. After eight consecutive years in the red, BCOM began to turn a profit in 2003 after diversifying into the auto-electronics business four years ago. (May 2005)

- Get to Know Us

- About Us

- Business Partners

- Follow Us on Facebook

- Services & Products

- Customized Sourcing Services

- Trade Magazines / eBooks

- Taiwan Industry Updates

- Global Trade Shows

- Global Pass

- Help

- FAQ

- Contact Us

- Site Map

©1995-2006 Copyright China Economic News Service All Rights Reserved.